Managing personal finances is a key pillar of the American Dream. Whether you are building your first budget, paying off debt, or investing for retirement, having a clear financial strategy can help you achieve stability and long-term freedom. In a country with diverse income levels, credit systems, and investment opportunities, financial education is more important than ever.

Below, we explore practical and proven financial principles tailored for Americans who want to take control of their money.

1. Build a Realistic Budget (Not a Perfect One)

A budget is not about restriction—it’s about direction. Many Americans struggle financially not because they earn too little, but because they don’t track where their money goes.

Key tips:

Use the 50/30/20 rule:

- 50% for needs (housing, food, transport)

- 30% for wants (entertainment, lifestyle)

- 20% for savings and investments

- Track expenses monthly using apps or spreadsheets

- Adjust your budget as your income or life changes

- Consistency matters more than perfection.

2. Master Credit and Debt Management

Credit plays a major role in the U.S. financial system. From credit cards to mortgages, how you manage debt directly impacts your credit score and future opportunities.

Smart debt strategies:

- Always pay at least the minimum on time

- Focus on paying high-interest debt first

- Keep credit utilization below 30%

- Avoid unnecessary consumer debt

- A strong credit profile can save you thousands of dollars in interest over your lifetime.

3. Create an Emergency Fund

Unexpected expenses—medical bills, car repairs, job loss—are common. An emergency fund acts as a financial safety net.

Recommended goal:

- Save 3 to 6 months of essential living expenses

- Keep the money in a high-yield savings account

- Use it only for true emergencies

- This habit alone can prevent financial stress and debt cycles.

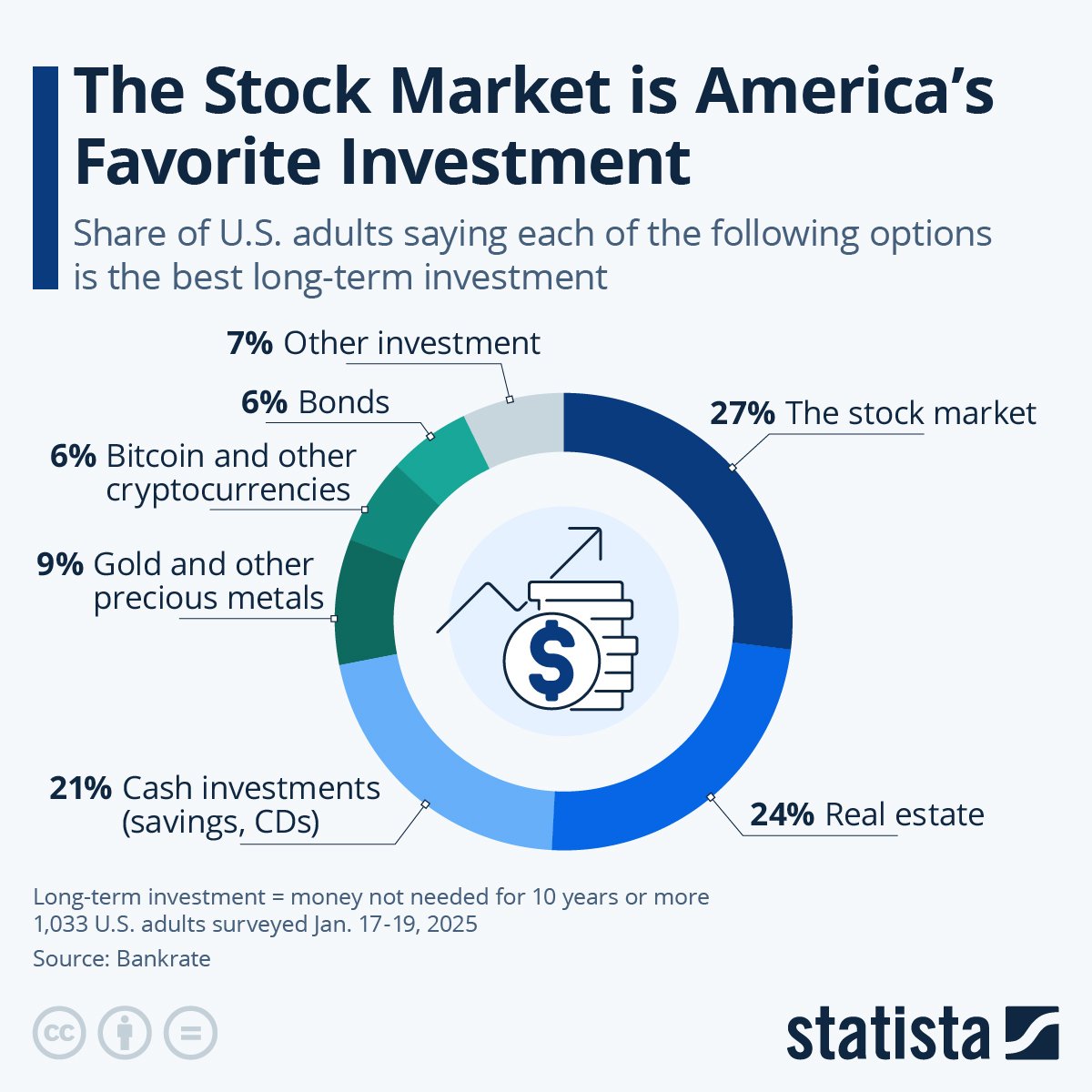

4. Start Investing Early (Even With Small Amounts)

Investing is one of the most powerful tools for building wealth in America. Thanks to compound interest, starting early is far more important than starting big.

Beginner-friendly options:

- Retirement accounts (like employer-sponsored plans or IRAs)

- Low-cost index funds

- Dollar-cost averaging instead of timing the market

- Time in the market beats timing the market.

5. Plan for Retirement With Intention

Many Americans underestimate how much they will need in retirement. Relying solely on government benefits is risky.

Smart retirement habits:

- Increase contributions when your income grows

- Take advantage of employer matches

- Diversify retirement investments

- Review your plan annually

- Retirement planning is not just for older adults—the earlier you start, the easier it becomes.

6. Increase Income, Not Just Savings

While budgeting and saving are important, increasing your income can dramatically accelerate financial growth.

Ideas to boost income:

- Develop high-demand skills

- Negotiate salary increases

- Start a side hustle or online business

- Invest in education or certifications

- Financial freedom often comes from combining smart money habits with income growth.

Final Thoughts

Personal finance is a lifelong journey, not a one-time decision. For Americans, understanding how money, credit, and investments work is essential to building stability and wealth in an increasingly complex economy.

Start small, stay consistent, and remember: every smart financial decision you make today brings you closer to a more secure tomorrow.